Cover CA health insurance plays a vital role in ensuring access to quality healthcare for California residents. This guide delves into the intricacies of navigating the state’s health insurance marketplace, empowering you to make informed decisions about your coverage.

From understanding the different plan types to exploring financial assistance options, we’ll provide comprehensive insights to help you find the right plan for your needs and budget.

California’s health insurance landscape is complex, with various plans and options available. We’ll explore the key features of each plan type, including HMOs, PPOs, and EPOs, and discuss the advantages and disadvantages of each. We’ll also shed light on the Affordable Care Act (ACA) and its impact on California health insurance, highlighting how it has expanded access to affordable coverage for many.

Understanding California Health Insurance

Navigating the world of California health insurance can be confusing, but it doesn’t have to be. This guide will help you understand the different types of plans available, their key features, and how the Affordable Care Act (ACA) affects your options.

Types of Health Insurance Plans in California

California offers a variety of health insurance plans to fit different needs and budgets. Understanding the differences between these plans is crucial for making an informed decision.

Covering your health insurance in California is crucial, as it provides peace of mind knowing you’re protected in case of unexpected medical needs. While focusing on physical well-being is important, it’s also inspiring to remember the inner beauty emphasized in verses like the one found on this website , which reminds us that true beauty goes beyond the physical.

With the right health insurance plan, you can focus on both your physical and inner well-being, knowing you have the financial support to navigate life’s unexpected turns.

- Health Maintenance Organizations (HMOs): HMOs provide comprehensive coverage within a specific network of doctors and hospitals. You typically need a referral from your primary care physician to see a specialist. HMOs generally have lower premiums than other plan types but may have higher out-of-pocket costs if you go outside the network.

- Preferred Provider Organizations (PPOs): PPOs offer more flexibility than HMOs. You can see any doctor or hospital, in-network or out-of-network, but you’ll pay a higher co-pay or coinsurance for out-of-network care. PPOs often have higher premiums than HMOs but lower out-of-pocket costs for in-network care.

- Exclusive Provider Organizations (EPOs): EPOs are similar to HMOs in that they require you to use a specific network of providers. However, unlike HMOs, EPOs do not require referrals for specialist visits. EPOs generally have lower premiums than PPOs but offer limited out-of-network coverage.

Key Features of Health Insurance Plans

When choosing a health insurance plan, consider these key features:

- Coverage: This refers to the medical services covered by the plan, such as doctor visits, hospital stays, prescription drugs, and preventive care. Plans vary in the types of services they cover, so carefully review the coverage details.

- Cost: The cost of a health insurance plan is determined by several factors, including your age, location, and health status. The plan’s premium, co-pays, and deductibles all contribute to the overall cost.

- Network Access: The network is the group of doctors, hospitals, and other healthcare providers that participate in the plan. Ensure the plan includes providers you need and are comfortable with.

The Affordable Care Act (ACA) and California Health Insurance

The ACA has significantly impacted California health insurance. Some key aspects include:

- Expanded Coverage: The ACA has expanded coverage to millions of Californians through subsidies and the creation of Covered California, the state’s health insurance marketplace. This expansion has reduced the number of uninsured individuals.

- Essential Health Benefits: The ACA mandates that all health insurance plans must cover ten essential health benefits, including preventive care, maternity care, and mental health services. This ensures that all individuals have access to essential healthcare services.

- Prohibition of Pre-Existing Conditions: The ACA prohibits health insurance companies from denying coverage or charging higher premiums based on pre-existing medical conditions. This ensures that everyone has access to affordable health insurance regardless of their health history.

Navigating the California Health Insurance Marketplace

Covered California, the state’s health insurance marketplace, simplifies the process of finding and enrolling in health insurance. It offers a range of plans from different insurance companies, allowing you to compare options and choose the best fit for your needs and budget.

Applying for Health Insurance Through Covered California

The application process is straightforward and can be completed online, by phone, or in person.

- Create an Account:Begin by creating an account on the Covered California website. This allows you to save your information and track your application progress.

- Provide Personal Information:You’ll need to provide basic personal details, including your name, address, Social Security number, and income information. This information is used to determine your eligibility for financial assistance and to calculate your premium costs.

- Select Your Coverage:Covered California offers a variety of plans with different levels of coverage and costs. You can compare plans based on factors like premiums, deductibles, and co-pays to find the best fit for your needs and budget.

- Enroll in Your Plan:Once you’ve chosen a plan, you can enroll online or by phone. You’ll receive confirmation of your enrollment and information about your coverage.

Comparing Health Insurance Plans

Understanding the different factors involved in health insurance plans is crucial for making an informed decision.

- Premiums:Premiums are the monthly payments you make for your health insurance coverage. They can vary depending on factors like your age, location, and chosen plan.

- Deductibles:A deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. The higher your deductible, the lower your monthly premium will typically be.

- Co-pays:Co-pays are fixed amounts you pay for specific medical services, such as doctor visits or prescriptions.

- Co-insurance:Co-insurance is a percentage of the cost of medical services that you pay after you’ve met your deductible.

- Out-of-Pocket Maximum:The out-of-pocket maximum is the most you’ll have to pay for covered medical services in a year. Once you reach this limit, your insurance will cover 100% of the remaining costs.

Finding the Most Affordable and Comprehensive Plan

Covered California offers several tools and resources to help you find the most affordable and comprehensive plan based on your individual needs and circumstances.

- Plan Comparison Tool:The Covered California website features a plan comparison tool that allows you to compare plans side-by-side based on factors like premiums, deductibles, and co-pays.

- Eligibility for Financial Assistance:Covered California offers financial assistance to help people afford health insurance. You can use the website’s eligibility calculator to see if you qualify for subsidies or tax credits.

- Enroll During Open Enrollment:Covered California’s open enrollment period typically runs from November 1st to January 31st. During this time, you can enroll in a new plan or change your existing plan.

Essential Considerations for Choosing Coverage

Choosing the right health insurance plan is a crucial decision that can significantly impact your financial well-being and access to healthcare. It’s essential to carefully consider your individual needs, medical history, and anticipated healthcare expenses to make an informed choice.

Understanding Your Health Needs and Medical History

Before exploring available plans, it’s vital to understand your individual health needs and medical history. This includes factors like:

- Pre-existing conditions:If you have a pre-existing condition, such as diabetes, asthma, or heart disease, it’s essential to choose a plan that covers the necessary treatments and medications.

- Expected healthcare utilization:Consider how often you typically visit doctors, specialists, and hospitals. If you anticipate frequent healthcare visits, you may need a plan with lower deductibles and copayments.

- Prescription medications:If you take regular medications, ensure your chosen plan covers the drugs you need at an affordable cost.

Key Factors to Consider

Several key factors influence your choice of health insurance plan. These include:

- Age:Age is a significant factor, as healthcare costs tend to increase with age. Younger individuals may opt for lower-cost plans with higher deductibles, while older individuals may prefer plans with more comprehensive coverage and lower out-of-pocket expenses.

- Health Status:Your current health status is another crucial consideration. If you are generally healthy, you might choose a plan with lower premiums but higher deductibles. However, if you have chronic health conditions or anticipate significant healthcare needs, a plan with lower out-of-pocket costs and comprehensive coverage may be more suitable.

- Anticipated Medical Expenses:Consider your potential medical expenses based on your health history, family history, and lifestyle. If you anticipate significant medical costs, a plan with lower deductibles and copayments might be a better choice.

Determining the Appropriate Level of Coverage and Benefits

Once you’ve assessed your individual needs and considered key factors, you can start evaluating different plans. The following steps can help you determine the appropriate level of coverage and benefits:

- Review plan details:Carefully examine each plan’s coverage details, including deductibles, copayments, coinsurance, and out-of-pocket maximums. These elements define your financial responsibility for healthcare services.

- Compare networks:Ensure your preferred doctors and hospitals are included in the plan’s network. Out-of-network care can be significantly more expensive.

- Evaluate benefits:Assess the plan’s benefits, such as coverage for preventive care, mental health services, and prescription drugs.

- Consider premium costs:Balance the plan’s coverage and benefits with its monthly premium cost. Choose a plan that offers the best value for your needs and budget.

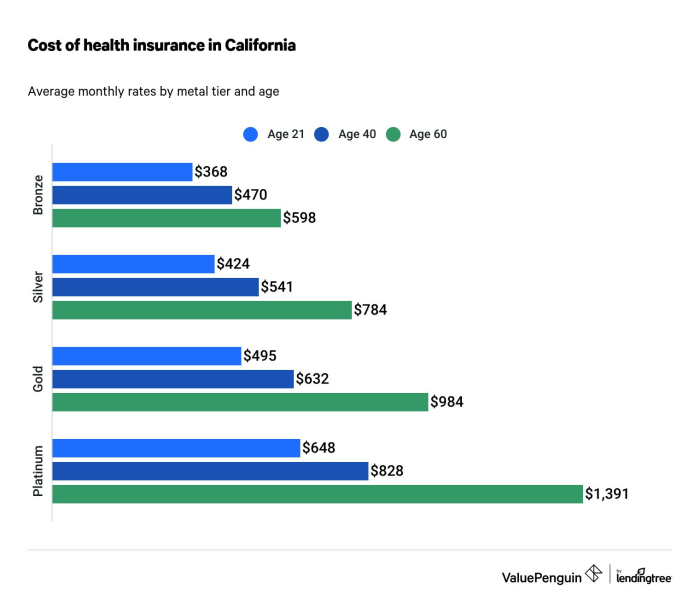

Financial Aspects of Health Insurance

Navigating the cost of health insurance in California can be complex, but understanding the financial aspects can make it more manageable. The state offers various subsidies and financial assistance programs designed to make health insurance more affordable for residents.

Financial Assistance Programs

Financial assistance programs are available to help Californians afford health insurance. These programs can significantly reduce monthly premiums and out-of-pocket costs.

Subsidies

Subsidies are financial assistance provided by the government to lower the cost of health insurance premiums. These subsidies are available through the Covered California marketplace and are based on income and family size.

The amount of subsidy you receive depends on your household income, the number of people in your household, and the cost of health insurance plans in your area.

Covering your health insurance in California is crucial, especially if you’re active and enjoy staying fit. A great place to get your fitness fix is CAP Fitness , which offers a variety of classes and equipment to suit all levels.

Remember, maintaining your health is an investment in your overall well-being, and having adequate health insurance can provide peace of mind in case of any unexpected medical needs.

Cost-Sharing Reductions

Cost-sharing reductions are available to help reduce your out-of-pocket costs, such as deductibles, copayments, and coinsurance. These reductions are available to individuals and families with lower incomes and are offered through the Covered California marketplace.

Cost-sharing reductions are calculated based on your income level and the cost of your health insurance plan.

Other Financial Assistance

Besides subsidies and cost-sharing reductions, other financial assistance programs may be available. These programs can help with things like deductibles, copayments, and other healthcare expenses.

- Cal MediConnect:This program helps eligible seniors and people with disabilities who have both Medicare and Medi-Cal.

- Medi-Cal:This program provides low-cost or no-cost health insurance to eligible Californians.

- Prescription Drug Assistance Programs:These programs can help reduce the cost of prescription drugs.

Eligibility for Financial Assistance

Eligibility for financial assistance programs is based on several factors, including income level and family size.

Income Level

Your income level is the primary factor determining your eligibility for financial assistance. Income limits vary based on family size and the type of financial assistance you are seeking.

You can use the Covered California website to determine if you qualify for subsidies or cost-sharing reductions based on your income.

Family Size

Your family size also plays a role in determining your eligibility for financial assistance. The larger your family, the higher your income limit for qualifying for assistance.

The Covered California website provides a tool to calculate your estimated monthly premium and determine your eligibility for financial assistance based on your income and family size.

Understanding Coverage and Benefits

When choosing a health insurance plan in California, understanding the coverage and benefits is crucial. This section delves into the essential components of California health insurance plans, including the types of benefits offered, the variations in coverage across plan types, and the financial aspects you need to consider.

Types of Benefits

The benefits offered in California health insurance plans are designed to cover a wide range of medical needs. These benefits typically include:

- Preventive Care:This category covers routine checkups, screenings, and vaccinations designed to prevent illnesses. Preventive care is often covered at 100% with no co-pay or deductible, emphasizing the importance of early detection and disease prevention.

- Hospitalization:This covers inpatient care, including room and board, surgery, and other medical services received during a hospital stay. Coverage for hospitalization varies by plan, with some plans requiring higher co-pays or deductibles than others.

- Prescription Drugs:Most plans offer coverage for prescription medications. However, the specific drugs covered and the associated costs can vary significantly depending on the formulary (a list of covered drugs) and the tier of the drug (which reflects its cost).

- Mental Health and Substance Use Disorder Services:California health insurance plans are required to provide comprehensive coverage for mental health and substance use disorder services. This includes therapy, counseling, medication, and inpatient treatment.

- Emergency Care:All plans cover emergency services, ensuring access to critical care in urgent situations. It’s important to note that emergency services received out-of-network may require higher out-of-pocket costs.

Coverage Differences by Plan Type

California health insurance plans are categorized into different types, each with its own set of coverage characteristics and costs. Understanding these differences is crucial for choosing the plan that best suits your needs and budget.

Covering your health insurance in Canada is a vital step in ensuring peace of mind. It allows you to access quality healthcare without the worry of exorbitant costs. But beyond the practicalities, remember that life is full of beautiful moments, like a breathtaking sunset or the laughter of loved ones.

These moments remind us of the beauty that exists all around us, just like all the beauty in the world that’s waiting to be discovered. So, take care of your health insurance, and then go out and experience all that life has to offer.

- Health Maintenance Organization (HMO):HMO plans typically offer lower monthly premiums but require you to choose a primary care physician (PCP) within their network. You’ll generally need a referral from your PCP to see specialists or receive certain services.

- Preferred Provider Organization (PPO):PPO plans offer more flexibility than HMOs. You can choose to see doctors both in and out of the network, but you’ll pay lower costs for in-network care. PPOs typically have higher monthly premiums than HMOs.

- Point-of-Service (POS):POS plans combine features of HMOs and PPOs. You’ll need to choose a PCP within the network, but you can also access out-of-network care with higher costs. POS plans offer a balance between cost and flexibility.

- Exclusive Provider Organization (EPO):EPO plans are similar to HMOs, requiring you to use providers within the network. However, unlike HMOs, EPOs generally do not allow you to see out-of-network providers, even in emergencies. EPOs often have lower monthly premiums than PPOs.

Provider Networks, Cover ca health insurance

Each health insurance plan has a provider network, which is a group of doctors, hospitals, and other healthcare providers who have agreed to provide services to plan members at negotiated rates. It’s essential to choose a plan with a provider network that includes doctors and hospitals you trust and are convenient for you.

- In-Network Providers:When you see a provider within your plan’s network, you’ll pay the negotiated rate, which is typically lower than the usual out-of-pocket cost.

- Out-of-Network Providers:Seeing a provider outside of your network may result in significantly higher costs. You may be required to pay a higher co-pay, deductible, or a portion of the bill yourself.

Co-pays, Deductibles, and Out-of-Pocket Maximums

Understanding the financial aspects of your health insurance plan is crucial for budgeting and managing your healthcare expenses. These terms are essential to know:

- Co-pay:A fixed amount you pay for certain medical services, such as a doctor’s visit or a prescription.

- Deductible:The amount you pay out-of-pocket before your insurance coverage kicks in for covered services.

- Out-of-Pocket Maximum:The maximum amount you’ll pay out-of-pocket for covered services in a year. Once you reach this limit, your insurance will cover 100% of the remaining costs.

Example:Imagine your plan has a $1,000 deductible and a $3,000 out-of-pocket maximum. If you incur $2,000 in medical expenses, you’ll pay the first $1,000 (deductible) and your insurance will cover the remaining $1,000. However, if your medical expenses reach $4,000, you’ll pay the $1,000 deductible and $2,000 more, reaching your out-of-pocket maximum.

After that, your insurance will cover all remaining costs for the rest of the year.

Resources and Support

Navigating the world of health insurance can feel overwhelming, but you’re not alone. California offers a wealth of resources to help you find the right coverage and understand your options.

Covered California

Covered California is the official health insurance marketplace for California. It provides a one-stop shop for individuals and families to compare plans, enroll in coverage, and access financial assistance. Covered California offers several resources to support consumers, including:

- Online enrollment platform:Covered California’s website provides a user-friendly platform for browsing plans, comparing prices, and enrolling in coverage.

- Phone assistance:Covered California operates a call center staffed with trained professionals who can answer your questions and guide you through the enrollment process. Their number is 1-800-300-1506.

- In-person assistance:Covered California has a network of certified enrollment counselors who can provide personalized guidance and support. You can find an enrollment counselor near you using the Covered California website.

- Resources for specific populations:Covered California offers resources tailored to specific populations, such as seniors, immigrants, and individuals with disabilities.

Insurance Brokers

Insurance brokers are licensed professionals who can help you compare health insurance plans from different insurers. They can provide personalized advice and guidance based on your individual needs and budget. To find a broker near you, you can use the Covered California website or the California Department of Insurance website.

- Personalized guidance:Brokers can help you understand your options and choose a plan that meets your specific needs.

- Plan comparison:Brokers can compare plans from different insurers, highlighting key features and benefits.

- Enrollment assistance:Brokers can assist you with the enrollment process and ensure that you have the right coverage.

Consumer Advocacy Organizations

Consumer advocacy organizations work to protect the rights of consumers and advocate for fair and affordable health insurance. These organizations can provide information, resources, and support to individuals seeking health insurance.

- Consumer Reports:Consumer Reports is a non-profit organization that provides independent reviews and ratings of consumer products and services, including health insurance plans.

- California Health Advocates:California Health Advocates is a non-profit organization that provides free legal and advocacy services to consumers with health insurance issues.

- Health Access:Health Access is a non-profit organization that advocates for affordable and accessible health care for all Californians. They offer resources and information on a range of health insurance topics.

Online Resources

The internet offers a wealth of information and resources for individuals seeking health insurance.

- Covered California website:The Covered California website is a great starting point for researching health insurance plans and enrolling in coverage.

- California Department of Insurance website:The California Department of Insurance website provides information on health insurance regulations, consumer rights, and complaints.

- HealthCare.gov:HealthCare.gov is the federal health insurance marketplace. While it focuses on national coverage, it provides valuable information and resources for individuals seeking health insurance.

- Consumer Reports website:Consumer Reports provides independent reviews and ratings of health insurance plans, helping you compare different options.

Last Point

Choosing the right health insurance plan can be a daunting task, but with the right knowledge and resources, it doesn’t have to be overwhelming. By understanding your individual health needs, exploring financial assistance options, and comparing plans carefully, you can find a plan that provides comprehensive coverage at an affordable price.

This guide serves as your roadmap to navigating the California health insurance landscape and securing the peace of mind that comes with knowing you have access to quality healthcare.

Frequently Asked Questions: Cover Ca Health Insurance

What is the difference between an HMO and a PPO?

An HMO (Health Maintenance Organization) typically requires you to choose a primary care physician (PCP) within the network. You need a referral from your PCP to see specialists. PPOs (Preferred Provider Organizations) offer more flexibility, allowing you to see specialists without a referral, although costs may be higher if you go outside the network.

How do I know if I qualify for financial assistance?

Eligibility for financial assistance is based on your income and family size. You can use Covered California’s online tool to estimate your eligibility and potential savings.

What are the key factors to consider when choosing a health insurance plan?

Consider your health needs, medical history, age, budget, and preferred provider network. It’s also important to compare premiums, deductibles, co-pays, and out-of-pocket maximums.