Health insurance major is a critical aspect of personal and family well-being, providing financial protection against unexpected medical expenses. Understanding the different types of plans, key considerations for choosing the right one, and navigating the health insurance market is crucial for individuals and families seeking peace of mind and financial stability.

This guide explores the fundamentals of health insurance, including the importance of coverage, the various plan options available, and factors to consider when selecting a plan. We’ll also delve into the role of major insurance companies and discuss emerging trends shaping the future of health insurance.

The Importance of Health Insurance

In today’s world, health insurance is more than just a financial product; it’s a crucial safety net that safeguards your well-being and financial stability. It provides peace of mind, knowing that you have a financial cushion to rely on in case of unexpected medical emergencies.

Financial Security

Health insurance offers a vital financial safety net by covering a significant portion of your medical expenses, protecting you from potentially devastating financial burdens. Unexpected illnesses or injuries can lead to exorbitant medical bills, including hospitalization, surgeries, and long-term care. Without adequate health insurance, these costs can quickly deplete your savings, leave you with substantial debt, and even jeopardize your financial security.

Peace of Mind

Having health insurance provides peace of mind, allowing you to focus on your health and recovery without the added stress of worrying about medical costs. Knowing that your insurance will cover a substantial portion of your medical expenses allows you to make informed decisions about your treatment and care without financial constraints.

Choosing the right health insurance major can be a daunting task, especially when you consider the various factors like coverage, cost, and network. If you’re in New Jersey and have Horizon NJ Health, finding a doctor within your network is crucial. You can easily locate a doctor by using the convenient online tool available at find doctor horizon nj health.

This tool helps you quickly find a qualified doctor in your area, making your health insurance major more valuable.

Examples of Medical Events

Here are some examples of common medical events that can lead to significant financial burdens without adequate health insurance:

- Hospitalization: A stay in the hospital, even for a short period, can generate substantial bills for room and board, medical services, and medications.

- Surgeries: Surgical procedures, from routine to complex, involve significant costs for the surgeon’s fees, operating room charges, and post-operative care.

- Chronic Conditions: Managing chronic conditions like diabetes, heart disease, or cancer requires ongoing medical care, medications, and specialized treatments, all of which can be expensive.

- Accidents: Accidents, whether at home, work, or while traveling, can result in injuries requiring emergency care, hospitalization, and rehabilitation, leading to substantial medical expenses.

Types of Health Insurance Plans

Choosing the right health insurance plan can be overwhelming, given the wide array of options available. Understanding the different types of plans and their features is crucial to make an informed decision that best suits your needs and budget.

Individual Plans

Individual health insurance plans are purchased directly by individuals, separate from any employer-sponsored coverage. These plans provide coverage to the individual and their dependents.

| Plan Type | Key Features | Benefits | Limitations |

|---|---|---|---|

| Individual Plans | Purchased by individuals, not tied to employment. | Flexibility in choosing plans, coverage options, and providers. | Potentially higher premiums compared to group plans. |

Group Plans

Group health insurance plans are offered through employers, unions, or other associations. These plans are often more affordable than individual plans due to economies of scale.

| Plan Type | Key Features | Benefits | Limitations |

|---|---|---|---|

| Group Plans | Offered through employers, unions, or associations. | Lower premiums compared to individual plans, often with more coverage options. | Limited flexibility in choosing plans and providers. |

Medicare

Medicare is a government-sponsored health insurance program for individuals aged 65 and older, as well as younger individuals with certain disabilities.

| Plan Type | Key Features | Benefits | Limitations |

|---|---|---|---|

| Medicare | Government-sponsored health insurance for individuals aged 65 and older. | Comprehensive coverage for medical expenses, including hospital stays, doctor visits, and prescription drugs. | Eligibility requirements based on age or disability. |

Medicaid

Medicaid is another government-sponsored health insurance program, providing coverage for low-income individuals and families.

| Plan Type | Key Features | Benefits | Limitations |

|---|---|---|---|

| Medicaid | Government-sponsored health insurance for low-income individuals and families. | Affordable or free coverage for medical expenses, including doctor visits, hospital stays, and prescription drugs. | Eligibility requirements based on income and family size. |

Key Considerations for Choosing a Plan

Choosing the right health insurance plan is crucial for protecting yourself and your family from unexpected medical expenses. Several factors influence the decision-making process, and it’s essential to carefully evaluate each aspect to ensure you select a plan that meets your individual needs and budget.

Coverage, Health insurance major

Coverage refers to the specific medical services included in your health insurance plan. It’s essential to understand what services are covered and what limitations might exist.

- Deductibles: The amount you pay out-of-pocket before your insurance coverage kicks in.

- Copayments: Fixed amounts you pay for specific services, like doctor visits or prescriptions.

- Coinsurance: A percentage of the cost of covered services you pay after meeting your deductible.

It’s vital to consider your typical healthcare needs and potential future medical expenses when assessing coverage. For instance, if you have chronic health conditions, you’ll want to ensure your plan covers the necessary treatments and medications.

Health insurance is a major part of financial planning, and it’s essential to choose a plan that fits your individual needs. One provider to consider is Aetna Better Health of Kansas , which offers a variety of plans for different income levels and health situations. By researching different options, you can find the best health insurance major for your unique circumstances.

Premiums

Premiums represent the monthly cost of your health insurance plan. They can vary significantly depending on factors such as age, location, and plan type.

- Plan Type: Different plan types, such as HMOs, PPOs, and EPOs, have varying premium structures.

- Coverage Level: Higher coverage levels generally come with higher premiums.

- Individual vs. Family Coverage: Family coverage typically costs more than individual coverage.

It’s essential to balance your budget with the level of coverage you need. Consider your financial situation and compare premiums across different plans to find the most affordable option that meets your requirements.

Network

The network refers to the group of doctors, hospitals, and other healthcare providers that your health insurance plan covers.

- In-Network Providers: Healthcare providers within the network offer discounted rates to plan members.

- Out-of-Network Providers: Healthcare providers outside the network may not be covered by your plan, or you might face higher costs.

It’s crucial to ensure your preferred doctors and hospitals are part of the plan’s network to avoid unexpected out-of-pocket expenses.

Pre-existing Conditions

Pre-existing conditions refer to medical conditions you had before enrolling in a health insurance plan.

- Coverage for Pre-existing Conditions: The Affordable Care Act (ACA) prohibits insurance companies from denying coverage or charging higher premiums based on pre-existing conditions.

- Waiting Periods: Some plans might have waiting periods before covering pre-existing conditions.

If you have pre-existing conditions, it’s essential to understand how your chosen plan handles them and whether any waiting periods apply.

Benefits

Health insurance plans often offer additional benefits beyond basic medical coverage.

- Dental Coverage: Covers dental services, such as cleanings, fillings, and extractions.

- Vision Coverage: Covers eye exams, glasses, and contact lenses.

- Prescription Drug Coverage: Covers the cost of prescription medications.

These additional benefits can significantly impact the overall cost of your healthcare. Consider your individual needs and budget when evaluating these benefits.

Navigating the Health Insurance Market

The process of obtaining health insurance can seem daunting, but understanding the key steps and resources available can make it more manageable. Here’s a breakdown of the process:

Open Enrollment

Open enrollment is a designated period when individuals can sign up for or change their health insurance plans. The open enrollment period for individual health insurance plans offered through the Health Insurance Marketplace typically runs from November 1st to January 15th of each year. During this time, individuals can shop for plans, compare coverage options, and enroll in a plan that meets their needs.

Health Insurance Marketplace

The Health Insurance Marketplace is an online platform where individuals can compare and purchase health insurance plans. The Marketplace offers plans from different insurance companies, allowing individuals to find the best coverage and price for their needs. The Marketplace is also a great resource for individuals who are eligible for financial assistance, such as tax credits to help offset the cost of premiums.

Insurance Brokers

Insurance brokers are professionals who can help individuals find the best health insurance plan for their needs. Brokers have access to a wide range of plans from different insurance companies and can provide expert advice on the best options for individuals based on their specific circumstances. Brokers can also help individuals navigate the enrollment process and ensure they are enrolled in the right plan.

The Role of Major Insurance Companies

Major health insurance companies play a significant role in the US healthcare system, providing coverage to millions of Americans. They act as intermediaries between individuals and healthcare providers, facilitating access to medical services while managing costs.

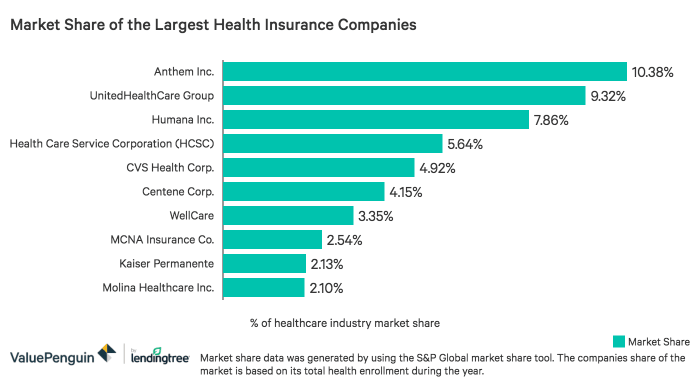

Overview of Major Health Insurance Companies

These companies are responsible for a substantial portion of the health insurance market in the US, each offering a wide range of plans and services to meet diverse needs.

Health insurance majors often delve into the complexities of healthcare systems, but they might not always consider the role of physical activity in mental well-being. A study published in the Journal of Behavioral Medicine found that regular exercise can be as effective as medication for mild to moderate depression, suggesting that incorporating fitness for depression into health insurance plans could be a valuable addition.

This approach aligns with the growing trend towards holistic healthcare and could lead to significant cost savings in the long run.

- Anthem is one of the largest health insurance companies in the US, serving over 40 million members. It offers a comprehensive range of plans, including individual, family, and employer-sponsored coverage. Anthem is known for its strong network of healthcare providers and its focus on preventive care.

- UnitedHealthcare, a subsidiary of UnitedHealth Group, is the largest health insurer in the US, with over 50 million members. It offers a broad spectrum of plans, including individual, family, Medicare, and Medicaid coverage. UnitedHealthcare is known for its extensive network of providers and its focus on cost-effective care.

- Cigna is a global health service company with a strong presence in the US. It offers a wide range of health insurance plans, including individual, family, and employer-sponsored coverage. Cigna is known for its focus on health and wellness programs, and its emphasis on personalized care.

- Humana specializes in Medicare and Medicaid coverage, serving over 4 million members. It offers a variety of plans, including individual, family, and employer-sponsored coverage. Humana is known for its focus on senior care and its commitment to providing affordable healthcare.

- Aetna, a subsidiary of CVS Health, is a major health insurance company with a strong presence in the US. It offers a wide range of plans, including individual, family, and employer-sponsored coverage. Aetna is known for its focus on quality care and its commitment to improving patient outcomes.

Future Trends in Health Insurance: Health Insurance Major

The health insurance industry is constantly evolving, driven by technological advancements, changing consumer preferences, and a growing focus on value-based care. These trends are shaping the future of how individuals access and pay for healthcare.

Telemedicine

Telemedicine, the use of technology to provide remote medical care, is rapidly gaining traction. It offers convenience, accessibility, and cost-effectiveness, particularly for patients in rural areas or with limited mobility.

- Virtual Consultations: Patients can connect with healthcare providers through video conferencing, phone calls, or messaging apps for diagnosis, treatment advice, and follow-up care.

- Remote Monitoring: Wearable devices and smartphone apps enable continuous monitoring of vital signs, allowing providers to intervene early and prevent complications.

- E-Prescriptions: Electronic prescriptions streamline the medication process, reducing errors and improving patient adherence.

Telemedicine is expected to become increasingly integrated into traditional healthcare systems, offering greater flexibility and affordability.

Value-Based Care

Value-based care models emphasize delivering high-quality care while controlling costs. Instead of simply paying for services rendered, these models incentivize providers to improve patient outcomes and manage overall healthcare spending.

- Bundled Payments: Providers receive a fixed payment for a specific episode of care, encouraging them to optimize resources and reduce unnecessary procedures.

- Accountable Care Organizations (ACOs): Groups of healthcare providers collaborate to coordinate care for a defined patient population, sharing financial rewards based on quality and efficiency metrics.

- Population Health Management: Health insurance companies and providers focus on managing the health of entire populations, identifying and addressing health risks proactively.

Value-based care is shifting the focus from volume to value, encouraging a more proactive and patient-centered approach to healthcare.

Personalized Medicine

Personalized medicine tailors medical treatments to individual patients’ needs and genetic profiles. This approach recognizes that one-size-fits-all treatments are not always effective and can lead to adverse effects.

- Genetic Testing: Analyzing an individual’s DNA can reveal genetic predispositions to certain diseases, enabling personalized preventive measures and targeted therapies.

- Precision Medicine: Developing treatments that are specifically tailored to a patient’s genetic makeup and disease characteristics, leading to more effective and less toxic therapies.

- Pharmacogenomics: Studying how an individual’s genetic makeup influences their response to medications, allowing for more effective drug selection and dosage.

Personalized medicine holds immense promise for improving patient outcomes, reducing side effects, and optimizing healthcare spending.

Navigating the complex world of health insurance can be daunting, but with careful research and planning, individuals can find the coverage that best suits their needs and budget. Understanding the importance of health insurance, exploring different plan options, and considering key factors like coverage, premiums, and network can empower individuals to make informed decisions about their health and financial well-being.

Question & Answer Hub

What are the main types of health insurance plans?

There are four main types of health insurance plans: individual plans, group plans, Medicare, and Medicaid. Each plan offers different coverage, benefits, and limitations.

How do I find a health insurance broker?

You can find a health insurance broker through online directories, recommendations from friends or family, or by contacting your state’s insurance department.

What is open enrollment?

Open enrollment is a period when individuals can sign up for or change their health insurance plans. It typically occurs annually, though specific dates vary by state and insurance provider.

What are some of the major health insurance companies in the US?

Some of the major health insurance companies in the US include Anthem, UnitedHealthcare, Cigna, Humana, and Aetna.