What is an insurance deductible health – What is an insurance deductible for health? It’s a key aspect of understanding your health insurance plan and how much you’ll pay out-of-pocket for healthcare services. Imagine this: you go to the doctor for a routine checkup, and the bill comes to $200.

If your health insurance plan has a $500 deductible, you’ll be responsible for paying the first $500 of medical expenses before your insurance kicks in. After you’ve met the deductible, your insurance will typically cover a percentage of the remaining costs, depending on your plan’s coverage.

Deductibles are a common feature of health insurance plans, and they play a crucial role in determining how much you pay for healthcare. Understanding deductibles is essential for making informed decisions about your health insurance coverage and managing your healthcare costs effectively.

Let’s delve deeper into the concept of deductibles and explore their implications for your health and finances.

Understanding Insurance Deductibles

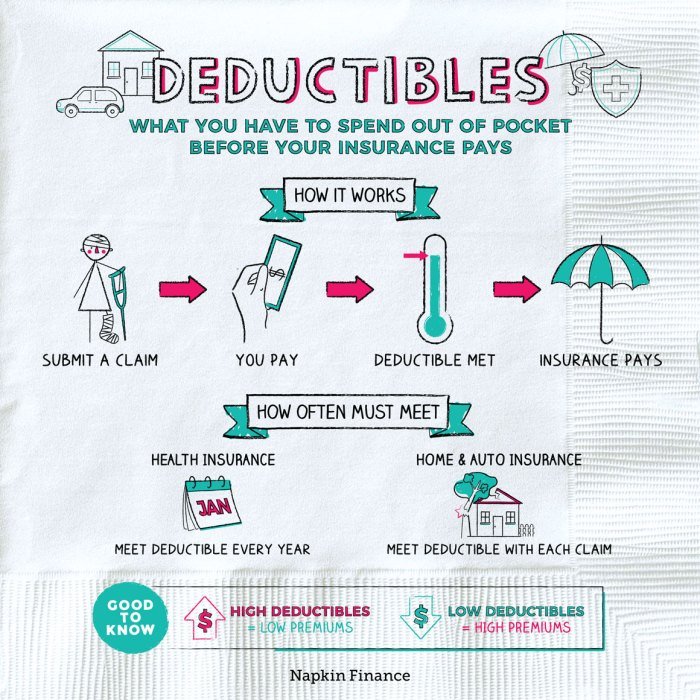

Imagine you have a car insurance policy with a $500 deductible. If you get into an accident, you’ll need to pay the first $500 of repair costs yourself. After that, your insurance company will cover the remaining expenses. This “first payment” you make is your deductible.

It’s a fixed amount you pay out of pocket before your insurance coverage kicks in.

Types of Deductibles, What is an insurance deductible health

Deductibles are a common feature in various insurance policies. They are not just limited to car insurance.

- Health Insurance:In health insurance, your deductible is the amount you pay for healthcare services (like doctor visits, hospital stays, or prescriptions) before your insurance coverage starts paying. For example, if you have a $1,000 deductible and incur $2,500 in medical expenses, you’ll pay the first $1,000, and your insurance will cover the remaining $1,500.

- Car Insurance:As mentioned earlier, car insurance deductibles apply to repairs after an accident. The higher your deductible, the lower your monthly premium, and vice versa. This is because the insurance company is taking on less risk if you agree to pay a larger portion of the costs yourself.

An insurance deductible health is the amount you pay out-of-pocket before your health insurance kicks in. It can be helpful to think of it as a way to share the cost of healthcare with your insurance company. For example, if you have a $1,000 deductible and you incur $2,000 in medical expenses, you would pay the first $1,000 and your insurance would cover the remaining $1,000.

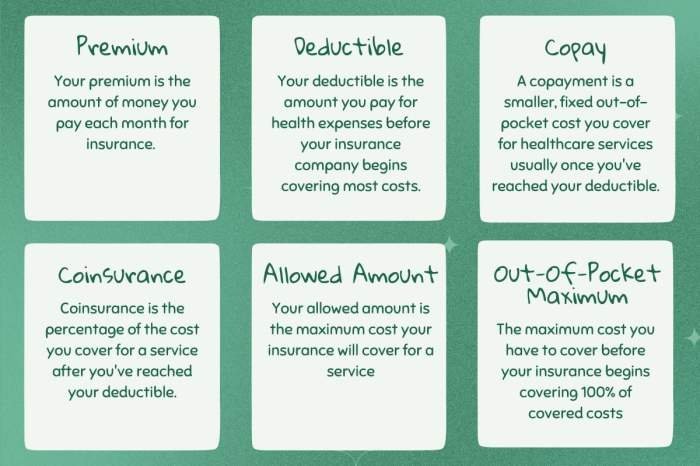

It’s important to note that deductibles are not the same as copayments, which are fixed amounts you pay for specific services. While you’re considering your health insurance options, it’s also a good idea to check out canas beauty for tips on maintaining a healthy lifestyle, which can help you minimize your healthcare costs in the long run.

- Homeowners Insurance:Homeowners insurance deductibles apply to damages caused by covered events like fire, theft, or natural disasters. You’ll pay the deductible before your insurance covers the rest of the repairs or replacement costs.

Deductibles in a Healthcare Setting

Let’s imagine you have a health insurance plan with a $500 deductible. You visit a doctor for a checkup, and the bill comes to $300. Since your deductible is $500, you’ll have to pay the entire $300 out of pocket.

However, if you later need to go to the hospital for a serious medical condition, and the bill is $10,000, you’ll pay the first $500 (your deductible), and your insurance will cover the remaining $9,500.

Health Insurance Deductibles

Deductibles are a common feature in health insurance plans. They represent the amount of money you must pay out-of-pocket for healthcare services before your insurance coverage kicks in. Understanding deductibles is crucial as they significantly impact your overall healthcare costs.

How Deductibles Affect Out-of-Pocket Costs

Deductibles directly influence your out-of-pocket expenses for healthcare services. When you incur medical expenses, you’ll first need to pay the deductible amount before your insurance coverage begins to pay for the remaining costs. For instance, if you have a $1,000 deductible and receive $2,000 worth of medical care, you’ll be responsible for the initial $1,000.

Your insurance will then cover the remaining $1,000, subject to your coinsurance and copayment obligations.

Types of Health Insurance Deductibles

There are different types of health insurance deductibles, each with its own implications for your out-of-pocket costs.

- Fixed Deductibles:Fixed deductibles are a predetermined amount that you pay each year, regardless of the number of medical services you utilize. For example, if your fixed deductible is $1,000, you’ll need to pay $1,000 in total before your insurance starts covering your medical expenses, even if you only visit the doctor once.

An insurance deductible is the amount you pay out-of-pocket before your health insurance plan kicks in. It’s a way to share the cost of healthcare with your insurer. Staying active can help you stay healthy and potentially lower your healthcare costs, which is why you might want to check out the delta fitness authority for fitness tips and resources.

Ultimately, understanding your insurance deductible and taking proactive steps to maintain your health can help you manage your healthcare expenses more effectively.

- Per-Incident Deductibles:Per-incident deductibles apply to each individual healthcare event. This means you pay the deductible amount for each separate instance of medical care you receive. For example, if your per-incident deductible is $500, you’ll pay $500 for each hospital visit or surgery, even if you have multiple services within the same year.

Factors Influencing Deductibles

Your health insurance deductible is the amount you pay out-of-pocket for covered healthcare services before your insurance starts paying. The deductible amount can vary significantly depending on several factors. Understanding these factors can help you choose a plan that best suits your needs and budget.

Factors Affecting Deductible Amounts

Several factors influence the amount of your health insurance deductible. These include:

- Plan Type: The type of health insurance plan you choose significantly impacts your deductible. For instance, Health Maintenance Organizations (HMOs) generally have lower deductibles than Preferred Provider Organizations (PPOs) or High Deductible Health Plans (HDHPs). HDHPs, designed for healthy individuals, often have the highest deductibles but lower monthly premiums.

- Age: Deductibles may increase with age, as older individuals tend to have higher healthcare costs. This is because older individuals are more likely to require more medical care due to age-related health conditions.

- Health Status: Your health status also influences your deductible. If you have pre-existing health conditions, your insurer may charge a higher deductible to reflect the potential for higher healthcare costs. This is because people with pre-existing conditions are more likely to require more medical care.

An insurance deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. It’s like a pre-payment for your health care, and it can vary depending on your plan. Imagine you’re looking for a new lipstick at a beauty storefront and you have a coupon for a certain percentage off.

That coupon is similar to your insurance coverage, but you still need to pay the initial amount before the discount applies. Similarly, with your health insurance, you pay the deductible first, and then your insurance covers the rest of your medical expenses.

- Location: The cost of healthcare varies depending on where you live. In areas with a higher cost of living, deductibles may be higher to reflect the increased costs of medical services.

- Family Size: Deductibles may also vary depending on the number of people covered under your plan. Family plans typically have higher deductibles than individual plans, reflecting the potential for higher healthcare costs for a larger family.

Deductible Comparisons Across Plans

The table below compares deductibles across different health insurance plans. Keep in mind that these are just general examples, and actual deductibles may vary depending on the specific plan and other factors.

| Plan Type | Individual Deductible | Family Deductible |

|---|---|---|

| HMO | $500 | $1,000 |

| PPO | $1,000 | $2,000 |

| HDHP | $1,500 | $3,000 |

Deductibles and Coverage

Your health insurance deductible directly influences the amount of coverage you receive. It’s the out-of-pocket amount you pay before your insurance plan starts covering medical expenses. Understanding how deductibles work is crucial when choosing a health insurance plan.

Deductibles and Coverage

The higher your deductible, the less your insurance plan will cover in the beginning. You’ll be responsible for paying more upfront before your coverage kicks in. Conversely, a lower deductible means you’ll pay less out-of-pocket initially, but your premiums might be higher.

For example, if your deductible is $1,000, you’ll need to pay the first $1,000 of your medical expenses yourself. After that, your insurance plan will start covering the remaining costs.

Deductibles and Copayments/Coinsurance

Deductibles are often paired with copayments or coinsurance. Copayments are fixed amounts you pay for specific services, such as doctor’s visits or prescriptions. Coinsurance is a percentage of the cost you pay after your deductible is met.

Let’s say you have a $1,000 deductible and a 20% coinsurance. If you incur $3,000 in medical expenses, you’ll pay the first $1,000 (deductible). After that, you’ll pay 20% of the remaining $2,000 ($400), and your insurance will cover the remaining $1,600.

Importance of Understanding Deductibles

Choosing a health insurance plan with a deductible that aligns with your needs and financial situation is essential. Consider factors such as your overall health, expected medical expenses, and budget.

- High Deductible Plansare often more affordable but require you to pay more out-of-pocket upfront. They are suitable for individuals who are generally healthy and expect low medical expenses.

- Low Deductible Plansoffer more immediate coverage but come with higher premiums. They are ideal for people who anticipate high medical costs or have pre-existing conditions.

Deductibles and Financial Planning

Deductibles are a crucial part of health insurance plans, influencing your out-of-pocket costs. Understanding how deductibles work and how they impact your finances is essential for making informed decisions about your healthcare.

Managing Out-of-Pocket Expenses

To effectively manage out-of-pocket expenses related to deductibles, consider these tips:

- Track Your Spending:Keep a detailed record of your healthcare expenses, including deductibles paid. This helps you monitor your progress towards meeting your deductible and identify areas where you can potentially save.

- Budget for Deductibles:Include your annual deductible in your annual budget. This ensures you have funds available to cover these costs when necessary.

- Consider a Health Savings Account (HSA):HSAs offer tax advantages for saving specifically for healthcare expenses, including deductibles.

- Negotiate Medical Bills:Don’t hesitate to negotiate medical bills, especially if you have a high deductible. Hospitals and providers are often willing to work with patients to reduce costs.

- Shop Around for Lower Deductibles:Compare different health insurance plans and consider plans with lower deductibles if it aligns with your budget and needs.

Saving Money for Deductibles

Saving money to cover deductibles is essential for managing your healthcare finances. Here are some effective strategies:

- Automate Savings:Set up automatic transfers from your checking account to a dedicated savings account for deductibles. This ensures consistent contributions without requiring manual effort.

- Reduce Spending:Identify areas where you can cut back on unnecessary expenses and allocate those funds to your deductible savings.

- Utilize Tax-Advantaged Accounts:HSAs offer tax benefits for saving specifically for healthcare expenses, including deductibles.

- Consider a Side Hustle:Generate additional income through a part-time job or freelance work to contribute to your deductible savings.

Impact on Overall Healthcare Costs

Deductibles can have a significant impact on your overall healthcare costs. Here’s how:

- Higher Out-of-Pocket Costs:Deductibles represent the amount you pay out-of-pocket before your insurance coverage kicks in. Higher deductibles mean higher initial costs.

- Potential for Financial Strain:Unexpected medical expenses can be financially challenging, especially if you have a high deductible.

- Impact on Utilization:Some individuals may delay or avoid necessary medical care due to concerns about high deductibles, potentially leading to more serious health issues later on.

Outcome Summary: What Is An Insurance Deductible Health

In conclusion, understanding insurance deductibles is essential for navigating the complexities of healthcare costs. By comprehending the role of deductibles in health insurance plans, you can make informed decisions about your coverage, manage your out-of-pocket expenses, and ensure that you have the financial resources to meet your healthcare needs.

Remember, deductibles are a crucial factor in determining your overall healthcare costs, so take the time to understand them thoroughly and choose a plan that aligns with your individual circumstances and budget.

Query Resolution

What happens if I don’t meet my deductible?

If you don’t meet your deductible, you’ll be responsible for paying the full cost of your healthcare services until you reach the deductible amount.

How do I know what my deductible is?

Your deductible is Artikeld in your health insurance plan documents. You can also contact your insurance provider for clarification.

Can I choose a plan with a lower deductible?

Yes, you can choose a plan with a lower deductible, but it will typically come with higher monthly premiums. It’s important to weigh the trade-offs between deductibles and premiums to find a plan that suits your needs and budget.

What are some strategies for saving money to cover my deductible?

Some strategies for saving money to cover your deductible include setting up a dedicated savings account, using a health savings account (HSA), or exploring options for employer-sponsored health plans.